English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mail Cited by SciELO

Cited by SciELO  Similars in

SciELO

Similars in

SciELO

Permalink

PermalinkIntroduction

The firewood production process for the generation of charcoal is worrisome from an environmental perspective, as currently, Brazilian states are not able to supply demand only with plantations, the most environmentally appropriate way to obtain this raw material (1). In the northeast, the reasons for the low success of planting tree species are water deficit, unfavourable soil conditions for plant growth and high initial investment costs (2). Thus, native vegetation takes on essential roles in the production of coal, offsetting inefficient plantations, which may reach 106 thousand hectares in 2020. The 40% dependence on areas of native vegetation to meet the demand required by the industrial and domestic sectors (3).

However, the production of firewood by native vegetation is most of the times illegal, without the standard measures of sustainable forest management (SFM) (2, 4), which results in clear cutting vegetation and high probability of conversion to pasture or agricultural areas. Resistance to FSM is mainly the result of the abundant supply of illegal wood and coal at low prices (5). The tendency is for illegality to decrease, according to the supply and inspection, causing companies to start adopting SFM for coal production. Therefore, for the citizen to be aware of the importance of SFM, it is crucial to carry out environmental, technical and economic studies that demonstrate viability, to guarantee the continuity of the production of firewood and charcoal by managed vegetation.

In the last twenty years, there has been a notable arrival of several steel industries for the production of pig iron, which has been installed along the "Carajás" railway, due to tax incentives and ease of obtaining raw materials (6). There was an increase in demand for coal to reduce iron ore, making firewood from native vegetation a necessary option, regardless of its origin. In the state of Maranhão, the coal comes from native vegetation or plantations. In plantations, greater initial capital and up to seven years are required for a return on investment, while in native areas, this revenue is achieved in the 2nd year (7). Some restrictions on the growth of the steel industries are supply uncertainties, legal and environmental risks and the lack of control of the price of charcoal in the market.

In other northeastern states, most are native vegetation, mainly the biome caatinga, or which is exploited illegally and has many plant species threatened with extinction due to strong extractive pressure from wood for wood production (1). The consumption of firewood occurs mainly by the ceramic industries and the domestic sector (2). The ceramic industries have an unsustainable energy base since more than half of the demand depends on firewood from native vegetation of the caatinga without SFM, which can prevent the long-term continuous production of firewood. This further reinforces the need for SFM projects to meet energy demands in the Northeast (1). The legal and bureaucratic requirements and uncertainties about the financial viability of SFM are the main factors that hinder the realization of sustainable projects (5, 6, 7 8).

Due to uncertainties regarding the SFM economy for coal production, it is necessary to make a financial assessment of the management system traditionally applied in the northeast region: the selective system (SS) and management in alternating bands system (MAB). We analysed MAB system with the objective of facilitating and making SFM more economical, as well as allowing the conservation of the caatinga biome, which is characteristic of the northeast and source of income for several traditional populations. From this context and the various management systems, the MAB system was tested to create an economically viable option for firewood production. A financial analysis was also performed comparing the results of the MAB with the SS carried out in the northeast region for coal production.

Materials and methods

Study area The study was carried out at the Annual Production Units 01 and 02 (APU 01 and 02), within the Forest Management Unit of the Magela Project (UMF-Magela) (04º35'20''S and 43º49'55.2''W), owned by the company Maranhão Gusa SA, municipality of Codó, state of Maranhão. The region's climate is Aw Koppen, with average annual precipitation and temperature of 28 ºC and 1 600 mm (9). The relief varies from flat to gently wavy, with a predominance of Yellow-Gray Latosol, with a sandy-clay texture and good permeability. The vegetation is classified as Open Ombrophilous Forest with two well-defined phytocenosis, namely: Open Ombrophilous Forest with Cipó and Open Ombrophilous Forest with Palm trees, which suffered small fires and unauthorized selective exploitation, with removal of fence posts and timber species of commercial value. (Tabebuia sp. and Cedrela sp.) (10).

Forestry systems APUs 01 and 02 were harvested, applying two silvicultural systems: alternate band management system (MAB) and selective management system (SS). The SS system divided work units into 50 m wide bands, which facilitated the control of harvesting activities. In this system, 90% of trees with DBH ( 8 cm were harvested, for a 30-year cutting cycle. The MAB system, originally called the strip-cutting system (BSC), was proposed to explore the forest by means of shallow cuts in the narrow bands, which are similar to natural disturbances in the forest, such as clearings caused by falling trees. In addition, this system is based on the following aspects: width of the strip, growth of natural regeneration, absence of fires and heavy machinery and cutting 30 to 70% of the total volume of the forest (10).

The change from BCS to MAB took into account the restrictions on forest use established in Normative Instruction No. 03/2001, which regulated the carrying out of management plans for the Northeast Region of Brazil during the period of MAB execution. The MAB started to be executed using bands of 75 m, which were subdivided into sub-bands of 50 (I) and 25 m (II), with the harvest being carried out first in sub-range I, while sub-bands II were preserved from cutting. Harvesting was carried out in sub-bands II according to the establishment of natural regeneration, proven by monitoring sub-bands I (10).

The width of the strips was two and a half times the average total dominant height of the forest (Hdom is equal to the average height of the 100 trees with the highest height in the inventoried sample), that is, L = 2.5 x Hdom. The strips were located in the field in a magnetic east-west direction, to maximize the incidence of light inside (10). In MAB, 60% of trees with 15 cm ≤ DBH <40 cm and 90% of trees with 15 cm> DBH ≥ 40 cm were harvested, for a 26-year cutting cycle. The use of these diametric classes was due to the fact that the remaining trees below 15 cm of DBH are often felled by the action of the wind or become bent, in addition to the shafts of trees above 40 cm of DBH have a high incidence of hollow in the Open Rainforest (10).

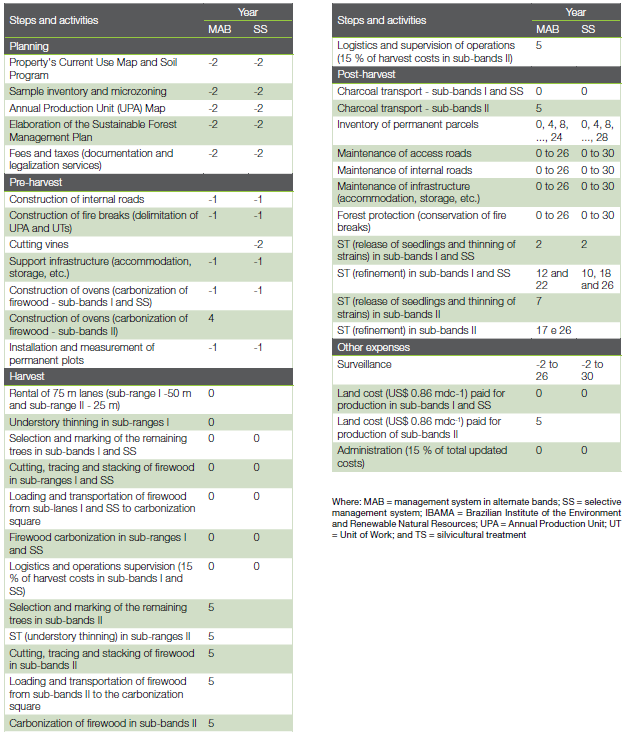

The matrix trees, in both systems, were selected considering the best phenotypic patterns (straight stem, without hollow, without termite and canopy in good phytosanitary condition and well distributed). They were not harvested: species that showed noble uses (cuttings and sawmills), those prohibited by law (Orbignya sp., Astronium sp. and Caryocar sp.) And those protected by their own act - for presenting, on average, less than one individual per hectare and three or more known uses. All individuals with these characteristics were elected as prohibited from cutting (10). The summary of the main activities carried out in the MAB and SS systems is in the topic ''Data collection, costs and production revenues''.

Data collection, production costs and revenues Three permanent plots of 50 x 200 m (1.0 ha) were installed, where the MAB and SS systems were applied. The pre-exploratory analysis showed that the plots installed in the MAB and SS systems have the same floristic composition and forest structure. These analyzes were described by Vieira et al. (11). This shows that the financial analysis were carried out considering the same initial condition.Raes

Labor costs (d-h), machinery, salaries, social charges (57.7% of salary), food, fuel, maintenance, depreciation of equipment, etc. were calculated. Throughout the cutting cycle, the different stages of vegetation succession offered diversified products, but the analyzes consider the revenues from the sale of post-plant coal, which occurred in the years 0 and 5 for the MAB system and 0 for the SS system. The cost-generating activities in both systems and their respective years of execution are described in Table 1.

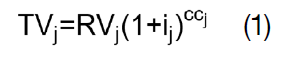

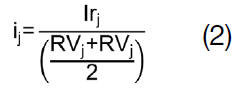

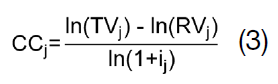

Cash flow The cash flow represents the costs and revenues distributed over the project's useful life (12). The planning horizon used, that is, the cutting cycle plus three years (planning phase, pre-harvest and harvest), was calculated using Equations 1, 2 and 3.

where: TVj = total or final stock volume in the j-th management alternative (m3‧ha-1); RVj = remaining stock volumein the j-th management alternative (m3‧ha-1); ij = annual growth rate in the j-th management alternative (%); CCj = cutting cycle in the j-th management alternative (years); Irj = average annual increase in the j-th management alternative; and ln = Neperian logarithm.

Financial Analysis The financial analysis evaluated whether the profit generated by the systems remunerates the invested capital. In this case, the evaluations were carried out using net present value for infinite horizon (NPV), estimated land value (ELV), equivalent annual value (EAV), benefit-cost ratio (BCR), Internal Rate of Return (IRR) and average production cost (APC) (12). An annual discount rate of 12% was considered for (13), which was also used to obtain the annual cost of land. Activity costs and product prices were obtained in March 2003, when the minimum wage in Brazil was R $ 240.00 (US$ 87.5). The dollar value in that same period was quoted at R $ 2.91 (14).

Sensitivity analysis The sensitivity analysis was carried out in two stages: the first considered the variation of the price of post-plant coal and forest productivity of ± 30% and the second, the variation only of the annual discount rate (6, 12, 18 and 24%).

Results and discussion

Complete floristic and structural analysis of the vegetation present in the evaluated forest management systems (MAB and SS) are available in previous studies (15), (11). The effects of using the MAB and SS systems on the structure and floristic composition of the vegetation were also evaluated in an open ombrophilous forest (11).

Composition of cost

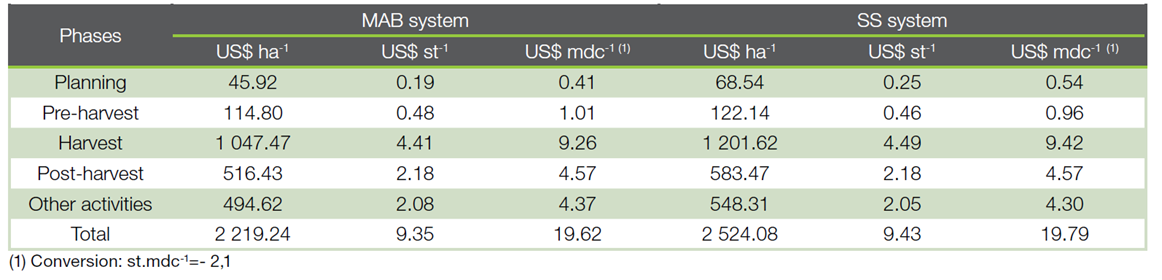

The total updated cost of the MAB system was US$ 2 219.24 ha-1, and that of the SS system was US$ 2 524.08 ha-1 (Table 2). In the MAB and SS systems, the total cost of planning activities was US$ 45.92 ha-1 and US$ 68.54 ha-1, respectively. Among these, the preparation of the Annual Operational Plan (POA) stood out, which was US$ 0.141 mdc-1 in the MAB system and the US$ 0.144 mdc-1 in the SS system. The highest cost of the SS system was due to the cutting of vines (US$ 0.141 mdc-1).

Table 2.Total cost updated in the different phases of MAB and SS system, MAGELA project, Codó municipality, Maranhão state, Brazil.

Barreto et al. (16) analyzed the production of wood under management in the region of Paragominas (PA) and estimated an exploration planning cost of US$ 72.0 ha-1 - approximately US$ 1.75 for each 6.26 m3, considering the exploitation of 35 to 40 m3‧ha-1. More than 90% of these costs were related to mapping trees, cutting vines and planning logging and logging operations.

Pre-harvest costs totalled US$ 114.80 ha-1 and the US$ 122.14 ha-1 in the MAB and SS systems, respectively. The cost item that stood out most in this stage was the construction of the ovens, which in MAB occurs in two different moments: sub-range I - one year before the harvest - and sub-range II - in year 4. In the SS system, the stage of construction of the ovens happens only in the first year. In the harvest, the largest capital investment occurred, 47.2% (US$ 1 047.47 ha-1) in the MAB system and 47.6% (US$ 1 201.62 ha-1) in the SS system. The production cost for firewood cutting and extraction was US$ 1.85 st-1 and US$ 1.12 st-1 in the MAB, respectively and US$ 2.05 st-1 and US$ 1.11 st-1 in the SS.

The carbonization cost for the two management systems was US$ 0.71 st-1. Even though the SS system does not require the location of a lane and silvicultural treatment (thinning of understory) in year 0, the productivity of the cutting team (chainsaw and auxiliary) was 13% lower. This reflected in the higher cost of coal in the harvest stage. In a forest management experiment for firewood and timber production in Buriticupu (MA), Jesus and Garcia (17) obtained harvest costs (firewood cutting and extraction) of US$ 3.80 st-1. This higher cost was due to the fact that the authors included costs for the pre- and post-harvest forest inventory.

In post-harvest, the cost was US$ 516.43 ha-1 and US$ 583.47 ha-1 in the MAB and SS systems, respectively. The cost item of this stage that required the greatest capital investment was transportation (US$ 3.16 mdc-1 up to 300 km) - approximately 16% of the current total cost in both management systems. The higher cost of the SS system was due to a longer cutting cycle, which resulted in increased maintenance activities. The other expenses (surveillance, land cost and administration) totalled US$ 494.62 ha-1 and US$ 548.31 ha-1 in the MAB and SS systems, respectively. This difference was due to the cost of the land, as the company reimburses the landowner only at harvest time, with a value of US$ 0.86 mdc-1. The land cost corresponded to 4.4 and 4.3% of the average production cost of the MAB and SS systems.

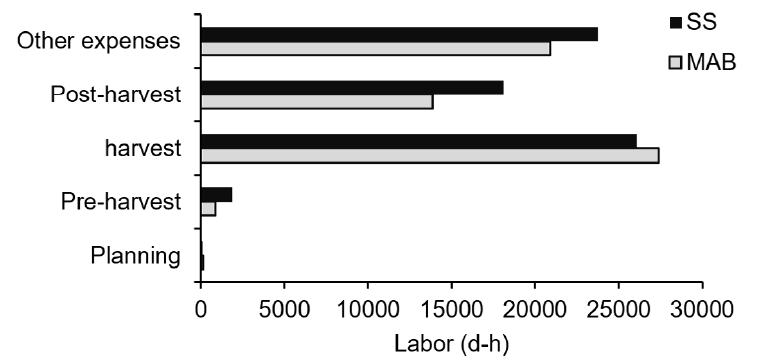

Labor During the planning stage, both systems required the same number of people (128 d-h). In the pre-harvest, labour was more significant in the SS system, due to the silvicultural treatment of cutting vines (4 d-h‧ha-1). At harvest, the MAB system employed more people due to the need to mark the strip (50 d-h‧ha-1) and thinning of understory (6 d-h‧ha-1). In post-harvest, the SS system demands more labour due to its longer cutting cycle (Figure 1).

Figure 1. Labor in the different phases of the MAB and SS systems, MAGELA project, Codó municipality, Maranhão state, Brazil.

Figura 1. Mano de obra en las diferentes fases de los sistemas MAB y SS, proyecto MAGELA, municipio Codó, estado Maranhão, Brasil.

In the SS system, it used 10.9% more hours of work, due to the long cutting cycle and lower harvest productivity of this system. However, the two systems generated practically the same demand for labour, 7.42 d-h‧ha-1‧year-1 and 7.23 d-h‧ha-1‧year-1 for the MAB and SS system, respectively. The MAB system provided a better distribution of labour throughout the cutting cycle due to the fact that silvicultural treatments and harvesting are carried out at different times (Figure 1). It is also worth mentioning that this study made work available to residents of the surrounding communities and the municipality of Codó. It also boosted the commercial sector of the municipality, through the acquisition of production tools, and contributed to local transportation, with the improvement of the road that gives access to the municipality's headquarters.

Cash flow The planning horizon for this financial analysis was the cut cycle plus three years (planning and pre-harvest phase). The cutting cycle was obtained with an average annual increase of 8.6 m3‧ha-1‧year-1 (18), as a result of cutting cycles of 26 and 30 years for the MAB and SS systems, respectively. According to Silva (19) the volumetric increment of all species in a SS system, with a high harvest rate, is between 5.7 and 8.6 m³ ha-1 year-1. Cash flows showed a profit (positive revenue) only at the harvest stage. In the MAB system, there was positive revenue in sub-band I in year 0 and sub-band II in year 5, while in the SS system there was only in year 0. With the sale price of post-mill coal equal to US$ 23.02 mdc-1, the current total revenue was US$ 2 603.70 ha-1 and US$ 2 936.01 ha-1 for the MAB and SS systems, respectively.

Financial analysis The MAB and SS systems are financially viable with a discount rate of 12% a.a.; that is, the discounted value of future revenues is higher than investments value (Table 3). The SS system, even with higher costs than the MAB, obtained better financial performance. The revenue is obtained in two moments, that is, years 0 and 5. As in year five, there is the effect of discount rate, the MAB system presented the lowest financial return.

Table 3. Net present value for infinite horizon (NPV), land expected value (LEV), equivalent annual value (EAV), benefit/cost ratio (BCR), internal rate of return (IRR), mean production cost (MPC), MAB and SS system, MAGELA project, Codó municipality, Maranhão.

In the SS system, the NPV of US$ 423.20 ha-1 was obtained, with the EAV of US$ 50.78 ha‧year-1, corresponding to 5.47% more profit than in the MAB system. NPVs annual discount rate at 12% in forest management for wood production would be US$ 480.0 and US$ 433.0 for 20 and 30 year cutting cycles, respectively (16) are higher than those estimated for charcoal production. Probably, projects that integrate wood production and coal production are more profitable.

The ELV (estimated land value) represents the maximum price that could be paid per hectare of land for management to be viable (12). In this way, as the SS system remunerated the capital better, you can pay more for the land, with a limit of up to US$ 552.63 ha-1. The average production cost of coal was US$ 0.17 mdc-1 higher in the SS system. The average profit was US$ 3.40 mdc-1 (17%) in the MAB system and US$ 3.23 mdc-1 (16%) in the SS system, at an average sale price of post-mill coal equal to US$ 23.02 mdc-1, coal produced from management systems can compete with coal from deforestation, sawmill waste and illegal exploitation. Barreto et al. (16) state that the management for wood production provides a profit of US$ 3.68 m-3, higher than that obtained with the production of coal.

Each US$ 1.0 invested will return financially as US$ 0.402 and US$ 0.398 for MAB and SS - BCR systems equal to 0.402 and 0.398, respectively. The annual IRR - the maximum discount rate that the project can support to remain viable - was 55.73% in MAB and 70.73% in SS. There is a large margin of safety for the systems on the interest rate practiced in the market to finance forest management. This annual interest rate does not exceed 10.7%. Although the SS system has good economic performance, it is a system that results in greater biomass removal (± 88% of the volume), as a consequence it will have less ecological viability (10, 20, 21). The MAB system has smaller removals (± 75% of the volume) and greater ecological viability for the management of Open Ombrophilous Forests for coal production (10).

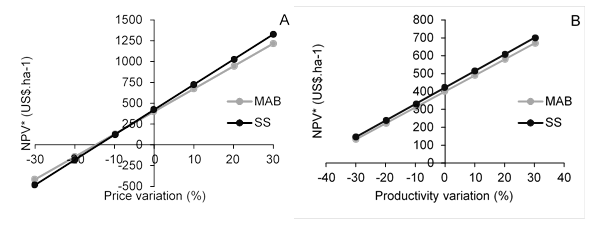

Sensitivity analysis

The MAB and SS systems are economically unviable when the annual discount rate is 12% and the -16% reductions in the price of post-mill coal. On the other hand, with variations of -10%, in the MAB there was a greater profit than that of the SS system. MAB can withstand small reductions in post-mill coal prices. However, the increase in the price of coal makes the SS system a more profitable management alternative, as there is greater appropriation of forest capital in the short term (Figure 2A). Regardless of productivity, the SS system provides greater economic return (Figure 2B) at an annual rate of 12%. In addition, the minimum production for economic viability is 92 and 72 mdc‧ha-1 for the MAB and SS systems, respectively.

Figure 2 Effect of percentage change in charcoal prices (A); forest productivity (B) in NPV (US$‧ha-1) of the MAB and SS systems, MAGELA project, Codó municipality, Maranhão state, Brazil

Figura 2. Efecto del cambio porcentual en los precios del carbón vegetal (A); productividad forestal (B) en NPV (US$ ha-1) de los sistemas MAB y SS, proyecto MAGELA, municipio de Codó, estado de Maranhão, Brasil.

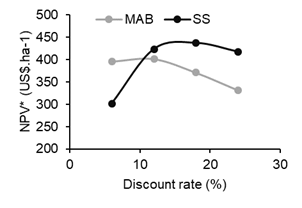

The MAB system is more economically attractive when there are lower discount rates (rates below 9.9% per annum). This performance is confirmed by the higher B/C ratio. The SS system increases profits up to a discount rate of 18% a.a., from that rate profitability tends to decrease (Figure 3).

Figure 3. Discount rate effect on the NPV (US$‧ha-1) of the MAB and SS systems, MAGELA project, Codó municipality, Maranhão state, Brazil.

Figura 3. Efecto de la tasa de descuento sobre el NPV (US$ ha-1) de los sistemas MAB y SS, proyecto MAGELA, municipio de Codó, estado de Maranhão, Brasil.

The financial performance of the MAB and SS systems was economically favorable, although few companies use them. There is a lack of knowledge of the benefits of these systems by executives in the steel industry, as well as disrespect for legislation and the facility to obtain charcoal from deforestation. Thus, if steel companies invest in sustainable management through the MAB and SS systems, they will be able to sustain a good part of their demand for charcoal and reduce financial uncertainties. Above all, these companies can provide social and economic development, generating employment for local populations. The resulting benefits will be: increase in productivity, reduction of waste and accidents at work, minimization of negative impacts and maintenance of forest cover and services resulting from it.

In addition to the benefits mentioned, forest management provides forest perpetuity and CO2 sequestration, which is commercialized in the form of carbon credits. In this context, forests are important for the carbon balance of the planet, because in vegetation and soil there is more carbon than there is an atmosphere today (22, 23). In forests managed by the MAB and SS systems, there was a periodic annual increase in volume of approximately 8.6 m3‧ha-1‧year-1 (18), these periodic increment data were obtained in analyzes on the effect of carbon credits in the economic viability of forest management. It would be possible to absorb 2.15 tC‧ha-1‧year-1, with an average estimate of carbon storage in wood of 0.25 tC‧m3 (24). Therefore, the adoption of a value of US$ 10.0 tC-1 (25) results in a potential revenue of US$ 21.5 ha‧year-1. When this annual revenue was included in the cash flows of the MB and SS systems, there was an increase of 24 and 33% in the NPV, respectively. Thus, the commercialization of carbon sequestered by managed forests will probably increase the profitability of forest management.

Conclusions

MAB and SS systems are financially viable. MAB is the best economic alternative, if the discount rate is less than 9.9%. The NPV varies depending on the discount rates. The MAB system had a good distribution of labor throughout the cut cycle, security of return on capital, return on investment, exceeding inflation and low degree of risk.

The charcoal on the market is most often of illegal origin. The steel industries must invest in the management of native forests to obtain charcoal in a sustainable way. This can reduce financial risks and provide social and economic development, with jobs and income for local populations