Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Enviar este artigo por email

Enviar este artigo por email Citado por SciELO

Citado por SciELO  Similares em

SciELO

Similares em

SciELO

Permalink

PermalinkIntroduction

In Brazil, the Mixed Ombrophilous Forest has forest remnants in the states of Rio Grande do Sul, Santa Catarina, Parana, Sao Paulo and Minas Gerais, being one of the most important ecosystems in the country. Among the tree species present in the mixed ombrophilous forest stand out the Araucaria angustifolia (Bertol.) Kuntze, Ocotea porosa (Nees) Barroso and Ilex paraguariensis A. St. -Hil. (1) or, in its popular name, yerba mate, which is of great environmental and socioeconomic importance for the southern region, stand out from Brazil, as it is its main non-timber forest product (2), (3).

The production of Brazilian yerba mate is the largest in the world and continues to increase due to the promotion of good prices, associated with technological advances for the herbaceous activity (4). The southern region of Brazil is the largest producer of yerba mate, in first place is the state of Parana, followed by the state of Santa Cataria and at last the state of Rio Grande do Sul. In addition to these three states there are, in the Brazilian Midwest, the state of Mato Grosso do Sul with a very small production in relation to the others and which has been decreasing every year (5).

As it is predominantly exploited by small producers, yerba mate has great social importance in Brazil (6), this culture is present in approximately 180 000 farms that feed around 600 yerba mate beneficiary companies and, generating approximately 700 000 jobs (7).

The leaves of yerba mate are used to prepare stimulating drinks, known as chimarrao, when consumed hot, or terere, when consumed cold (8), (9), besides serving for tea and as medicinal plant (10). It is a raw material for candies, caramels, ice cream, soft drinks, cosmetics, hygiene products, medicines, dyes, and detergents for hospital use (11). Despite these multiple products, chimarrao is the main form of consumption (12), (13).

Despite being a competitive product, farmers have traditionally invested little in planting maintenance, especially in terms of refill nutrients by fertilization. Regardless of the form of cultivation, conventional or organic, there is a need to fertilize the soil, since the raw material of the herb, composed of leaves and thin branches, removes from the soil a considerable amount of nutrients that needs to be replaced with periodic fertilization to avoid a drop in production at each harvest cycle (14).

The economic analysis of an investment involves the use of analysis techniques and criteria that compare costs and revenues inherent in the project, to decide whether or not it should be implemented or even modified (15). These analyzes should be based on cash flow, when the project has already been installed, or on financial projections for projects not yet executed (15), (16). Therefore, the investment evaluation study basically refers to the decisions of capital investments in projects that promise a return for several consecutive periods (17).

Yerba mate is a crop that responds very well to fertilization (14), but many producers, for fear of jeopardizing their profits, avoid it. Therefore, this research aimed to evaluate the economic effect of fertilization on yerba mate planting.

Material and methods

The two sites with yerba mate plantations are located on the northern plateau of the state of Santa Catarina, in the municipality of Tres Barras. In this region the soils are of medium to good fertility and predominantly clayey in texture (18). The first one, called Barra Grande Farm, is the experiment with fertilization in an area of 7.34 hectares, while the second one, called Capão Bonito Farm, is a 3.05 hectares plantation of that was carried out without any fertilization.

At Barra Grande farm, fertilization was carried out by applying 160 grams of poultry manure per seedling holes at planting and, from the second year, 85 grams of chemical fertilizer NPK (8-16-16) per plant were annually applied. This fertilization was recommended based on the nutritional demand of the crop, which is equivalent to that of corn and soybeans (14), and the supply of nutrients obtained from chemical analysis of the soil. Limestone was not applied because yerba mate tolerates soil acidity (19).

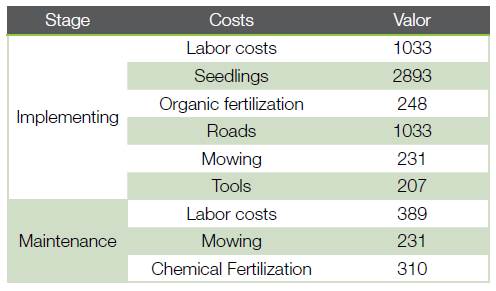

The economic study of costs is a widely debated subject and inserted in the planning of production activities (20). The costs of implementing planting with fertilization were summarized in the acquisition of seedlings, tools, organic fertilization, roads construction, mowing and labor costs, while in the maintenance stage were included costs of periodic chemical fertilization, mechanical mowing and labor costs. Table 1 shows the implementation and maintenance costs of a yerba mate hectare with fertilization, the case of Barra Grande Farm.

Table 1 Implementation and maintenance costs of fertilized yerba mate plantation per hectare in BRL (R$), Barra Grande Farm.

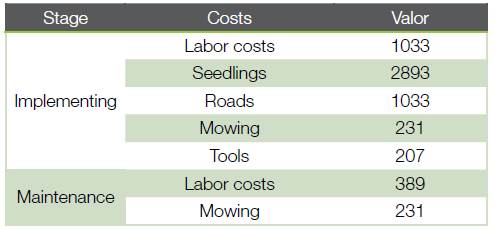

In a plantation without fertilization, the implementation costs were: seedlings acquisition tools, road construction, mowing and labor costs, in maintenance only mechanical mowing and labor costs appear. Table 2 shows the implementation and maintenance costs of a hectare yerba mate without fertilization, the case of Capão Bonito Farm.

Table 2 Implementation and maintenance costs of non-fertilized yerba mate plantation per hectare in BRL (R$), Capão Bonito Farm.

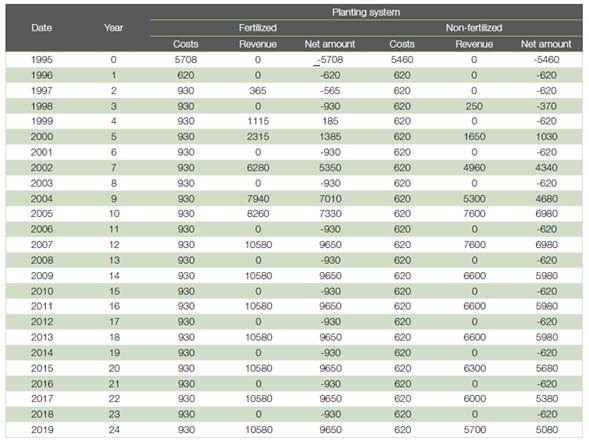

Table 3 shows the cash flows with all revenues and costs for the two sites over 25 years of investment. Over that time, the productivity of the fertilized area was 5821 kg ha-1 and the un fertilized area was 4882 kg ha-1.

For each site, the payback, revenue/cost ratio, average production cost, Net Present Value (NPV), infinite net present value (∞NPV), equivalent annual value (EAV), and the Internal

Rate of Return (IRR) were calculated.

Payback, or time to return on capital, stands out for its simplicity and broad economic utility (17) and consists of verifying which project has the shortest return on capital, that is, the time required for the sum of the revenue equals to the sum of costs. The payback is the ratio of the initial capital invested to the average cash flow result (15).

To calculate the revenue/costs ratio, the nominal sum of revenues that occur during the project’s useful life was divided by the nominal sum of costs. Thus, the higher the value of the ratio, the more interesting the investment option will be and, of course, ratio smaller than one are considered economically unviable (15).

The average production cost refers to the cost of production for each standard unit produced, this value was found by dividing the sum of the total costs obtained in the end of the investment by the total production in the end of the investment (15). The lower this cost, the more viable the investment is. The three economic methods described have restrictions for long-term investment, especially when this investment is installed in countries that do not have stable inflation, such as Brazil, as they do not consider the variation of capital over time.

Therefore, it is necessary to carry out other economic analyzes, like NPV, ∞NPV and VAE to confirm their results (15).

Regarding the term used to characterize capitalization or the decapitalization of revenues and costs in the economic evaluation, interest rate, discount rate and minimum attractiveness rate are used as synonyms (21). It is through this rate that future values are discounted to make them comparable values, or values are capitalized to make them comparable to future values (22). In forestry investments there is a great doubt related to the choice and use of discount rate (23). To solve this issue, four discount rates close to those applied to rural financing in Brazil were used to evaluate investments: 3, 6, 8 and 10 %.

The NPV consists of bringing to the zero date, which is the present date, all the cash flows of an investment and adding them to the initial value, that is, all the expenses that were made to start the project. NPV is defined by the current value of benefits less the current value of expenses (15), (16). Equation 1, below, represents the NPV calculation.

Where. NPV: net present value; Rj: current value of revenues; Cj: current cost value; i: minimum attractiveness rate; j: period in which revenues or costs occur; and n: maximum number of periods.

In the net present value method, the attractiveness rate is the discount percentage of cash flows. When the present value of the inflows minus the cash outflows is positive, there is a technical indication of acceptance of the investment. Otherwise, the investment must be rejected (17).

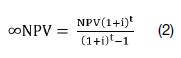

The ∞NPV considers the replication of a project in an infinite horizon (24). Equation 2, below, shows the ∞NPV calculation.

Where. ∞NPV: infinite net present value; NPV: net present value; i: minimum attractiveness rate; t: number of capitalization periods; and n: maximum number of periods.

Like the NPV, the project that presents the positive ∞NPV is economically viable, and the one with the highest ∞NPV is considered the best (24).

The EAV is the periodic portion related to the payment of an amount equal to the NPV of the investment option under analysis over its useful life (24), (25). The EAV analysis transforms the current value of the project, that is, the NPV, into a revenue stream or periodic and continuous costs, equivalent to the current value, during the life of the Project (24). Equation 3 below shows the EAV calculation.

Where EAV: equivalent annual value; NPV: net present value; i: minimum attractiveness rate; t: number of capitalization periods; and n: maximum number of periods.

The project will be considered economically viable if it presents positive EAV, indicating that the periodic benefits are greater than the periodic costs. As for the selection of options, the one with the highest EAV for a given discount rate should be chosen (15).

The IRR is the discount rate that equates the current value of future revenues with the current value of future costs of the project, constituting a relative measure that reflects the increase in the value of the investment over time based on resources required to produce the revenue stream (22), (26). The project will be financially viable when the IRR is greater than the minimum attractiveness rate (15). Due to its simplicity and applicability, IRR is perhaps the most used technique for evaluating investment alternatives (17). Equation 4 represents the IRR calculation:

Where. IRR: internal rate of return; Rj: current value of revenues; Cj: current cost value; j: period in which revenues or costs occur and n: maximum number of periods.

Results and discussions

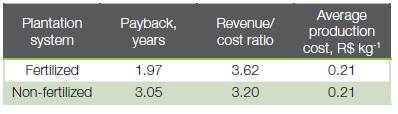

Table 4 shows the payback values in years, the ratio of the revenue used and the average production of one kilogram of yerba mate in both planting systems.

The fertilized planting system was the one with the shortest payback, showing that in this system the initial investment will return more quickly than the non-fertilized system, due to the higher revenues caused by increased productivity. So, when fertilization was chosen, the financial return happened one year earlier than the non-fertilized planting.

Considering the revenue/cost ratio, the most economically interesting planting system was also fertilizer, which showed the best value due to higher revenues. Despite the difference in results, all planting systems had a high revenue/cost ratio. The average production costs for all systems were close, but the cheapest way to produce yerba mate was fertilizing, this value represents the minimum selling price for the project to find its breakeven point, zero profit and zero money loss (17).

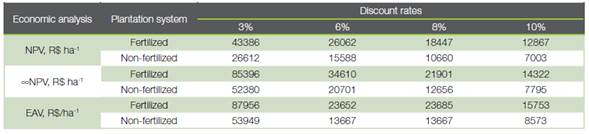

Table 5 shows the remuneration values for the capital invested in the two planting systems at the different annual discount rates employed.

Table 5 Earnings of the planting systems calculated by NPV, ∞NPV and EAV in four different discount rates.

All economic indicators (NPV, ∞NPV and EAV) pointed out that for any discount rates, the best performing planting system was that one with fertilization. The two planting systems were sensitive to rates, and it is possible to see falls in the assessment criteria as they increased. However, in no simulated scenario was an economically unfeasible situation found, that was, no negative evaluation criteria were found (27).

It is worth mentioning the importance of social financing programs promoted by the government, as in the case of the Brazilian Family Agriculture Support Program (PRONAF) (28), which offers loans to small rural producers under subsidized interest rates of 3.0 to 4.6 % per year. The production of yerba mate is mostly carried out by small rural producers (7), in this context, programs such PRONAF are suitable to boost the production of this non-wood forest product.

The IRR is an intrinsic rate to the project and does not depend on the minimum rate of attractiveness, it can be interpreted as the average growth rate of an investment (15), and therefore, the fertilized planting system was the best, as it has the highest IRR (Table 6).

Furthermore, the investment is considered economically viable when its IRR is higher than the discount rates applied (22), and the two planting systems had higher IRRs than the discount rates applied.

The growth and production of yerba mate biomass respond positively to the greater availability of K and P in the soil (29), and this greater supply of nutrients caused the best response in all the economic parameters analyzed. In addition to economic advantages, periodic nutritional replacement avoids soil depletion, as many years of harvesting without fertilization can reduce, or make the farm’s production capacity unviable (19).

Conclusions

When the planting of yerba mate was fertilized, despite the higher cost of implantation and maintenance, the average producing cost of one kilo of yerba mate was lower, so, the increase in the production that fertilization causes in the planting was significantly large and makes up for its expenses. The response of the fertilization also promoted the shortest payback and the biggest revenue/cost ratio.

The production of yerba mate was economically viable with or without fertilization, even in the higher applied discount rate, however in all economic indicators the fertilized planting system had better results, in addition to preventing soil nutritional exhaustion.